‘That’s China Speed.’ One of the most striking things about our recent visit to China was the pace at which everything is operating. This phrase, versions of which we kept hearing across companies that we were speaking with, underlined just how quickly the world’s second-largest economy is developing and how quickly companies are moving relative to their peers elsewhere. One of the most striking examples of this was in the breakneck pace of electric vehicle (EV) development. In the United States and Europe, it can take more than five years to develop a new passenger vehicle model; in China this can be as fast as eight months1. In the year to October 2025 the top three EV brands in China had approval for 83 new models, Volkswagen for six and Nissan for two2.

On this trip we spent two weeks in China, starting in Shanghai and moving down around the coast to finish up in Shenzhen and Hong Kong. We have previously found China to be both fascinating and a challenging place for us to find high-quality companies and were interested to see whether that would still be the case. Our biggest challenge is usually around alignment because of the government’s involvement in almost every company and its tight control of the economy and the incentives within it. We also find that the line between what is in the company and what is personal for some of the founders that we meet is somewhat blurred.

A Market Rich in Opportunity – and Impediment

From an entrepreneur’s perspective China is at the same time one of the best and one of the most challenging places to build a business. This is because of its largely homogeneous market where good ideas can grow very quickly, giving companies scale and experience that then allow them to compete overseas. The flip side of this is that it also results in hyper competition that both encourages innovation and severely tests competitive advantage. Where the government has an interest we also frequently come across significant subsidies, both in grants and in very low tax rates.

If you create a business that is in the country’s strategic interest, the government can be very generous, but this also creates sizeable risk. Unlike most countries we look at, in many ways companies in China become riskier as they get larger, because they find their way on to the central government’s radar. What the government wants and what is good for minority investors are not always aligned.

The Power of Brand

We have long liked companies with deep and wide competitive moats and for us brand is an interesting one. We noted on our last visit to China in mid-2024, how fierce competition made it appear that China had weaker brands than we see elsewhere. India appears to be in the process of demonstrating that as marketing and distribution advantages weaken, real branding power is exposed.

On this trip we met Foshan Haitian, a maker of soy and oyster sauce along with other condiments, almost like a Chinese Heinz. Here we found a brand that does appear to have loyalty, in part due to a long history that can’t be copied and a trust in the quality and consistency of a product. Nongfu Spring, China’s largest bottled water company, shows that this kind of trust does appeal to consumers.

We have admired Haitian over the years but found it difficult to understand its ownership, which put us off. Meeting them helped us better understand who sits above the listed business and certainly gave us some food for thought.

The challenges with the consumer space meant that we deliberately targeted many more industrial companies, from a maker of electrical relays, Hongfa Technology, to a manufacturer of hydraulic systems, Hengli Hydraulic. Industrial businesses tend to behave in very different ways from consumer staples, primarily because industrial cycles don’t affect whether people use soy sauce but do affect the end demand for electronics and excavators. In fact, because of inventory in the supply chain, this effect as you go further into the chain, tends to become more pronounced - like cracking a whip. The fact that these businesses can be deeply cyclical can actually create opportunities to buy them when they become unpopular in the short term. The advantage of being a long-term investor is that many businesses have compounded spectacularly over decades and even if our timing isn’t perfect when we first buy, we can have an opportunity later to buy more at an even better price.

The playbook for success for many of these companies is clear and repeatable. First find a successful and large business overseas in the industrial space. In China, they will typically offer the products that they have made for Western markets and will not be interested in tailoring for the Chinese markets. Then find one of their products that is relatively unsophisticated but has a high enough margin to enable you to produce and sell it at a discount of 15–20% to the existing alternative. If you can also offer customisation for local requirements then you probably have a winning offer. Scale this and then improve the technology to move up the value chain while using the scale to drive down cost. Eventually you will end up with the lowest cost and equivalent technology and will become the dominant player in China, which then allows you to go overseas.

Full Speed Ahead for EVs

As we travelled it was almost impossible to avoid the automotive supply chain. China has seen an explosion in electric vehicles over the past five years or so and there are now nearly 130 brands, with EVs making up over half of all cars sold. Why EVs? Chinese industrialists realised that they could not compete with European and American internal combustion engines, a technology refined and honed over many years. EVs, however, are a new platform with a level playing field. This is one of several examples where this has happened – others include solar technology, LiDAR and possibly robots, which we will return to later.

We met with Leapmotor, one of the challenger EV brands distinguished by its vertical integration. The history of this company explains why: its owner also owns the largest video surveillance company in China and is thus expert in the manufacture of electronics. Many of the founders of EV companies have a history in electronics, such as the phone manufacturer Huawei.

The scramble to gain market share is causing a phenomenon referred to as ‘involution’ or neijuan. In an industrial context this refers to a massive overinvestment in capacity which triggers self-destructive price wars and potential destabilisation of the value chain.

As we worked through the supply chain it became clear that these companies were in part funding themselves by using their suppliers. Although the car companies get paid up front by consumers, they take months to pay their suppliers. This builds a pool of cash that they can use to fund themselves. As a company grows it can continue to absorb cash in this way, but it relies on its suppliers remaining solvent and on demand continuing to grow. An unanswerable question we were left with was - how long can this house of cards continue? There was capacity in China last year to build 55.6m cars but only 27.6m cars were sold, which will probably result in at least some of this deflation being exported overseas3 – and also most likely far fewer car companies at some point in the future.

Electrifying Progress

Another consequence of this intense competition is that China is becoming an accidental green hero. As of August 2025 over half of all cars sold in China were either fully electric or hybrid. Pulling our lens back from just cars, an advantage China has over Western democracies is its time horizon. Xi Jinping is largely guaranteed to run the country for at least as long as he is able, which brings a certain stability and the ability to make longer-term strategic decisions about where to invest the country’s resources. Whereas the China of 20 years ago was copying and acquiring technology from foreign players, it is now a leader and an innovator in many domains. What these domains typically have in common is that they represent a technology shift where disruptors may have an advantage by not having a legacy that they need to manage (the core problem referred to in Clayton Christiansen’s The Innovator’s Dilemma).

A good example of this is in China’s recognition of and response to the long-term switch that is taking place from fossil fuels to renewable energy; it has the time horizons and control of incentives to become dominant in this new energy chain from rare earth metals to electric vehicles. The consequence is that China is rapidly altering its mix of production and consumption of energy and last year, according to the Global Energy Monitor, became one of the top 10 nations where renewable energy production exceeds fossil fuel.

Ironically, at the same time China has the highest installed capacity of coal power in the world, at over 50% of total global generation. The rapid rise and cost decrease in solar and wind haven’t stopped China having the largest backlog of new coal-fired power plants, with more capacity than the entire coal fleet of the US approved and entering construction (200 GW approved and 95+ under construction).

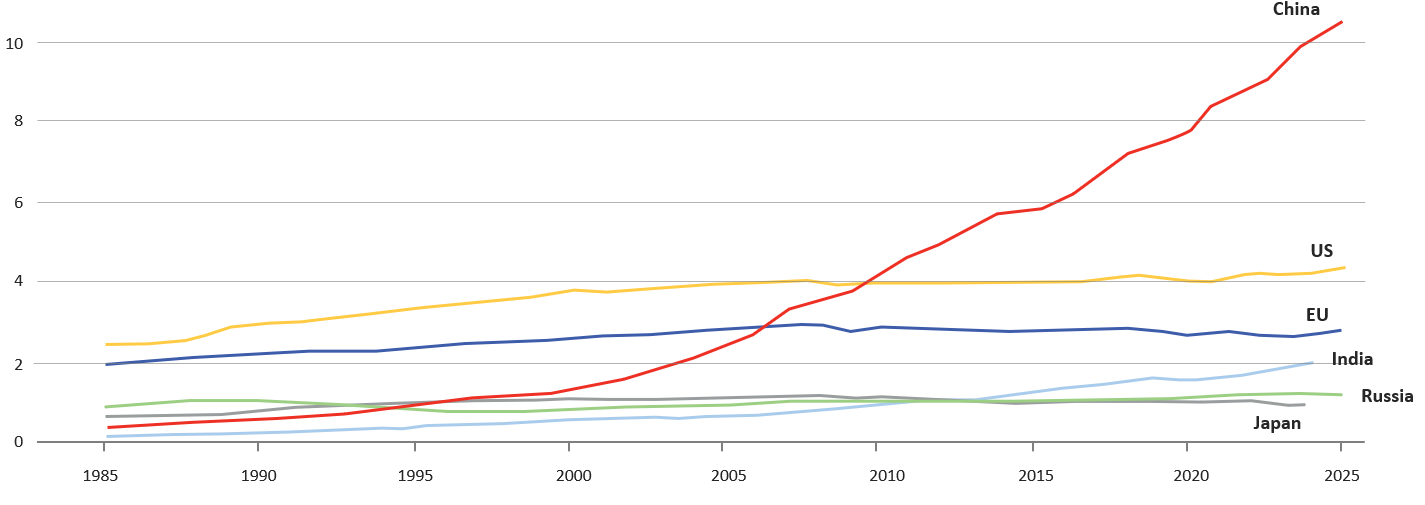

How do you reconcile these two seemingly opposing statistics? Simply by recognising that China is adding power at such a rate that it will add six times what America will over the next five years4. Why is this important? There are three reasons. First, AI is hugely power-hungry, and the US is already hitting limits on what the current infrastructure can support. Second, as recent events are demonstrating, dependence on others for your energy needs is a strategic weakness. And third, power capacity is needed not just for AI but also to power electric vehicles and, in the near future, an army of robots for manufacturing and, no doubt, other purposes. Chinese semiconductors still trail the leading edge of US-designed chips but stacking enough of them with enough power will get you a pretty similar result. We didn’t meet any semiconductor companies on this trip but did meet several companies that are the picks and shovels providing everything from power and packaging to the vast numbers of assembled servers that are required.

Plugging in

Electricity Generation – ‘000 TWh

Figure 1. China’s increased rate of electricity production will give it an advantage over the coming years.

Source: The Economist

Source: The Economist

It was obvious from our trip that the next big industrial wave to come out of China will be robotics and, like EVs, many companies see this as an opportunity and are finding ways to enter the industry in anticipation of a huge pickup in demand. Hengli Hydraulic is now making actuators for Tesla’s nascent robotics project. Midea, a manufacturer of air conditioners and other white goods, acquired KUKA, a German robotics company, in 2017. It has taken some time to integrate the two cultures but, having made progress in this, it positions a whole new leg for this business with the ability to build and refine for themselves given the scale of their white goods business.

Slowing Down to Reflect

Despite all this, as we gathered our thoughts on the trip it was impossible not to be struck by the number of governance issues we had come across. Investigating these forms a key part of our research before, during and after our trips. These risks are often ‘off-balance sheet’ and pose significant threats to minority investors, and we find, building out a picture of owners’ economic interests helps highlight misalignment. In one promising business we met, the chair owned three other companies outside the one we spoke to. We were told that if one ever ran into trouble the others could help. This clearly violates many of the principles surrounding a separately listed business.

In another we saw products with the company’s branding that were produced outside the listed company and owned separately by the chair. We were told not to worry, however, because the process for bringing this new technology into the business would be transparent.

Travel through China is always an interesting and educational experience. What exists there looks like capitalism but as you peel back the layers you realise that control and alignment are considered differently. Over time this can lead to very different outcomes for owners and minority shareholders, assuming in the first place that the owners are allowed to make a reasonable return. We have long maintained that our standard in every country needs to be similar and it is only by owning the best companies with aligned owners and management that we can generate acceptable returns over the long term. The trip brought us up to speed with some interesting investment ideas but also left us with a lot of questions that we still need to answer. Getting to a point where we have trust in a company takes time and a lot of slow work but there is no doubt that our time in China will prove fruitful.

1. Skerryvore company meetings.

2. Rest of World (19 November 2025). China is setting the pace in the EV race, and the West can’t keep up. https://restofworld.org/2025/china-us-ev-race

3. The German Autopreneur (26 September 2025). China builds 2x more cars than it can sell (China market update 2025). https://germanautopreneur.com/p/china-vs-west-auto-market-update-september-2025

4. The Economist (18 March 2026). Is cheap energy the key to China gaining AI supremacy? https://www.economist.com/china/2026/03/18/is-cheap-energy-the-key-to-china-gaining-ai-supremacy

Any information provided in this document relating to specific companies/securities should not be considered a recommendation to buy or sell any particular company/security.