'In a free enterprise, the community is not just another stakeholder in business, but is in fact the very purpose of its existence.’ – J.N. Tata (1839–1904)

Our investment philosophy has always been a straightforward one. We ask ourselves two seemingly simple questions – do we own high-quality businesses and are they available at an attractive price? Once we find a good business at a reasonable price we need the patience to sit on our hands and allow the company to deliver. Although we cannot predict the future we believe that good businesses will thrive over the long term.

Because our time horizon could extend beyond a decade, how a company treats all its stakeholders is of vital importance; the businesses we invest in have to be sustainable. The reputation of a business is what creates value beyond the machines in a factory, inventory in a warehouse or products on a shelf. A brilliant strategy will not save a company from consumers who don’t trust its products, talented employees who don’t want to work for its business or a government looking to halt damage to the environment.

Although the idea of sustainable investing is not new, a new form of what looks like sustainable investing has appeared in environmental, social and governance (ESG) investing. The end of the twentieth century and the beginning of this one have seen a dawning realisation that the way in which human beings live is in itself unsustainable. We cannot continue to consume in a way that pollutes the environment for future generations. Companies cannot continue to produce in a way that does not put back what they take out.

There is a complicated question around trading short-term profits for this longer-term gain, but the damage from the continuing emission of carbon dioxide, for example, will ultimately lead to diminished returns for every saver, let alone the societal and environmental consequences for the world.

ESG investing is a reaction to this and a recognition that those who allocate capital need to do so differently. It seeks to take three elements of a company’s relationship with its stakeholders and use them as a basis for investing. It is a narrower definition than what is implied by a sustainable company and often struggles to articulate the link between ESG and performance. The positive side of this is that it has raised awareness and almost every company we speak with has some response when we raise the topic of sustainability. Most companies are making progress but we see a number of problems with the direction the industry is headed in.

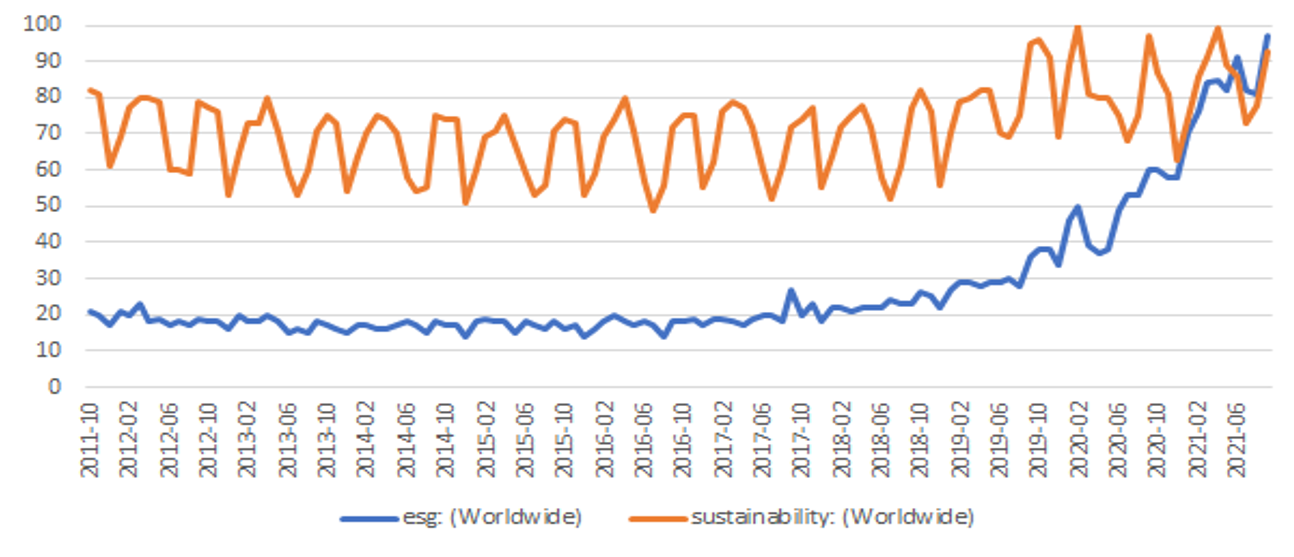

The interest in ESG has grown very rapidly since 2018 as money has poured into funds with assets passing $1.6 trillion in 2020[1]. Sensing this opportunity, the finance industry has seen an explosion in the availability of data on everything from carbon emissions to the gender make-up of workforces. But because the data is not standardised companies face an increasing burden in the form of custom questionnaires for data that is simply serving to create new profit pools for the oligopoly that controls financial information.

Figure 1: Google worldwide search popularity of ‘ESG’ and ‘sustainability’ from 2004 to 2021

Key considerations

There are a number of issues facing the current approach to ESG. The first is the focus on numbers and the formation of quantitative rules. The finance industry is full of tales of failed companies whose numbers, at least superficially, looked fine or even great. What the numbers don’t explain is whether a company is behaving sustainably. Worse still, producing numbers – especially ones that are unaudited and non-standardised – gives poor-quality managers and owners the opportunity to present their company as something it isn’t. ESG indexes (another new profit pool) include companies that we would never own because of how they behave, yet they find themselves passively held by savers trying to do the right thing. What these do allow, however, is passive funds to invest algorithmically, leading to some ridiculous outcomes that have nothing to do with a sustainable future.

The second issue is the emergence of thematic investing. This grossly oversimplifies or just ignores a more holistic view of a company if it happens to fit an easy-to-market theme. An example of this kind of failure is an emerging markets nickel mining business we have looked at. This company has been one of the world’s largest emitters of sulphur dioxide, a pollutant that has caused considerable harm to the people and environment around its plants[2]. The company is attempting to clean up its image and has committed to reducing its pollution but the record here suggests this may be more of a lick of paint than fundamental change. In the last two years the company has had a huge diesel spill into the local waterway from tanks that had not been adequately maintained[3], has been accused of taking bribes from a waste management supplier[4] and was responsible for the deaths of three of its employees last year after an accident in one of its processing plants[5].

Despite this track record the company is owned in several ESG funds because the metals its mines produce are required in increasing quantities in batteries used for the transition to a lower-carbon future. Surely the cure should not kill the patient in a different way?

The next issue is companies that move environmental liabilities ‘off balance sheet’ through omission or misdirection. We commonly see companies avoid the largest sustainability challenges they face by focusing on less material areas or avoiding discussing them at all. Four of the top 10 CO2 emitters worldwide are Indian resource companies[6]. One of these leads its most recent sustainability report with a goal of getting to zero carbon by 2035. But elsewhere it mentions that carbon emissions have actually gone up by 50% in the past four years because they are burning more coal. We also see consumer staples companies discuss solar panels installed on their offices (minor impact) but talk little about packaging and post-consumer waste (major impact). We find a strong correlation between companies that address their major challenges in an open way and the quality of the rest of the business.

Time is also a challenge. Many in the industry are rushing to create goals such as zero carbon in the portfolio or boards with specific diversity goals. The trouble is that making investment decisions driven by the latest fad does little to solve the problems that the world is facing and starves good companies of the capital they need to make changes.

Tata Power in India is an example of a company with excellent governance and social credentials but on today’s measures the business is a large emitter of carbon dioxide because it operates coal-burning plants. It is, however, committed to shutting these down by 2050[7] and is on its way to becoming one of the largest generators of renewable energy in the country. Yet, any portfolio that is measured on a carbon output basis would struggle to own a business that is key to the necessary change in India’s energy mix. Issues such as gender equality, diversity in workforces, reduction in carbon emissions and closed-loop manufacturing cannot be addressed overnight; they require time and patience, which the financial industry focused on quarterly results is not well equipped to provide.

The value of a business, a founder once told us, is created at the edges of the business in all the small decisions made by staff who are empowered and trusted to do the right thing. The current emphasis on boards and some of the arbitrary rules around what is and what is not acceptable are therefore unlikely to bring about better outcomes. A bad culture will win over a decent board because the board is too far away from the detail. The best boards we have found over the years are those that perform more of an advisory than an oversight role, which is why we object to arbitrary rules about how long a board member can serve, or a fixed percentage of independent directors. In many industries a long memory is more important than the hope a new board member uncovers a dastardly scheme. Far better to find a culture that prizes reputation, empowers and retains talented people and has either an owner whose family’s legacy is at stake or a culture that emulates this.

And then there’s engagement. This is a loosely defined term that can mean anything from asking polite questions about plastic packaging to working with other shareholders to force a vote on key matters. As shareholders we effectively engage with each portfolio company every time we are asked to vote, usually during their AGM. We, like many others in the industry, use the services of one of the two proxy voting companies that have created an unregulated oligopoly in proxy advisory. Importantly, we not only read the research provided, but we also always decide how to vote for ourselves, frequently based on conversations about any issues with the company.

We believe in building long-term relationships with management teams by behaving as thoughtful owners. We have found that constructive dialogue with the people controlling the company can be much more effective than voting anonymously from the shadows. A recent example of a corporate governance abuse in Indonesia, where the listed entity bought out another business from the controlling shareholder for an excessive price, provides an interesting case study. This transaction was a wanton abuse of shareholders and was called out in a well-written paper by a very large passive investor. The same shareholder unsuccessfully voted against the transaction but continued to own the shares, potentially exposing clients to future governance abuses.

Our approach

Our approach differs in that we tend to start from a position of trust, having done a large amount of due diligence on the management and owners of a company, looking at how they have behaved in the past – particularly during difficult times. We are backing the people running the company, so if we find ourselves voting against them we often have to ask ourselves tough questions about whether we have misjudged the quality of a business. We recently sold a bank from the portfolio after management tried to rewrite incentive targets in their favour because of the pandemic. We see many businesses that change the targets when external circumstances are bad but ‘forget’ to do the opposite in better times.

Over the years, we have tried to develop a set of principles to guide our investment in what we believe are sustainable companies. The paradox that many funds seem to wrestle with of incorporating ESG ‘overlays’ disappears when you believe that behaving sustainably is entirely consistent with generating better than average returns over the long term. There are a number of simple reasons for this outperformance that some of the more insightful management teams we have met over the years have outlined to us.

First, reputation matters. We once met the right-hand man of one of Asia’s richest people and asked what the key to his success was. The answer was simply that he cared about his reputation. When he did deals with people, he was smart enough to make much ‘better’ deals but chose not to, instead allowing both parties to come away with a fair deal. This was sustainable but also hugely rewarding because people began to actively seek him out to deal with in the future. Warren Buffett has also credited much of his success to being fair with people. Reputation also affects how customers and employees perceive you, how a government might treat you or the trouble an NGO might cause. All of these have significant long-term financial implications.

The second reason is competitive advantage. The expectations of stakeholders shift constantly. What was accepted 20 years ago was very different from what an employee or customer looks for today. A company that can position itself ahead of customers’ expectations can find itself in a space with very few competitors. Unilever is a good example of this kind of thinking, taking chemicals out of its products before consumers ask for it or, most recently, creating a strong purpose for its brands, which creates conversations in a world of social media and influencers.

Third, behaviour acts as an early warning system. The way a company treats its stakeholders can often foreshadow problems for investors. Indeed the whole concept of sustainability implies that a company that is not behaving this way will encounter a problem at some point. As disclosure has improved, spotting issues has become more subtle. Companies no longer admit the cost advantage of flouting environmental regulations (a real example) but may choose to omit the key sustainable issues from their reporting, instead drowning the reader in irrelevant detail.

Our guiding principles

At Skerryvore, we prefer to have a set of principles over simple targets as they better guide our decisions both in what we choose to invest in and how we run our business:

1. We will only own businesses we believe to be sustainable.

As with accounting data, sustainability metrics rarely tell the full story. We look at the why and the how behind the published numbers to better understand the behaviour of a company and whether this can be sustained.

2. We will seek far-sighted companies that recognise sustainability as an advantage.

We consistently find that the best companies recognise that behaving sustainably gives them a long-term advantage over those that do not. Most often this is to do with the power of a positive reputation and the benefits it confers.

3. We will seek to correct mistakes through engagement or divestment.

While we try before making an investment to avoid companies with sustainability-related issues, as we get to know companies over time we may come to realise that we have made a mistake. Where we can engage with the company to promote change we will attempt to do so but where this is not possible we will choose to sell.

4. We will actively engage with our companies to promote global best practices.

For a long time standards in companies have been relative – meeting the local laws or adhering to the country of domicile’s social norms. The most successful firms grow outside the country in which they started and to do so must judge themselves against the best companies globally. International investors are increasingly applying global standards to the firms they look at, so this can have a material effect on share price.

5. We will encourage better transparency and seek to work with those who promote it.

In general the direction of travel in terms of better disclosure is positive – but not all disclosure is useful. We will encourage the companies in which we invest to improve their disclosure so that it is comparable with the best globally and encourage facing up to and being open about the material challenges that operating sustainably presents.

6. We cannot ask companies to behave sustainably if we do not ourselves.

It is important that we live up to the standards that we encourage others to develop by looking closely at our business and seeking to make a positive impact.

[1] https://www.ft.com/content/7dd96b6d-26f5-48ed-b710-465f9fe5378d

[2] https://thebarentsobserver.com/en/2019/08/norilsk-tops-worlds-list-worst-so2-polluters

[3] https://www.dw.com/en/russian-nickel-mining-firm-admits-pollution-in-arctic/a-53976282

[4] https://tayga.info/170326

[5] https://www.newsmax.com/newsfront/processing-plant-arctic-deaths/2021/02/20/id/1010834/

[6] https://www.gonewsindia.com/latest-news/environment/12-indian-companies-among-worlds-top-100-co2-polluters-25867

[7] https://www.pv-magazine-india.com/2021/07/01/tata-power-to-exit-coal-by-2050/